A rural household runs on tight margins. Money enters in small waves and leaves in steady streams. Food, fuel, school costs, medicine, and loan payments do not wait for a “good month.”

This is why guaranteed support matters. A ration card or subsidy works like a fixed plank in a shaky bridge. It does not solve every problem, but it reduces the chance of a sudden fall.

Chance-based income works in the opposite way. It promises a big jump with a small stake. The outcome stays uncertain. Some days bring gain. Many days bring nothing. This pattern makes planning hard.

In this article, we will compare these two realities in simple terms. We will look at cash flow, risk, and household decisions. We will focus on what families can predict and what they cannot. We will treat “chance-based income” as a risk category, not as a moral issue.

Predictable Support Creates Planning Power

Planning begins with certainty. Even small certainty changes behavior.

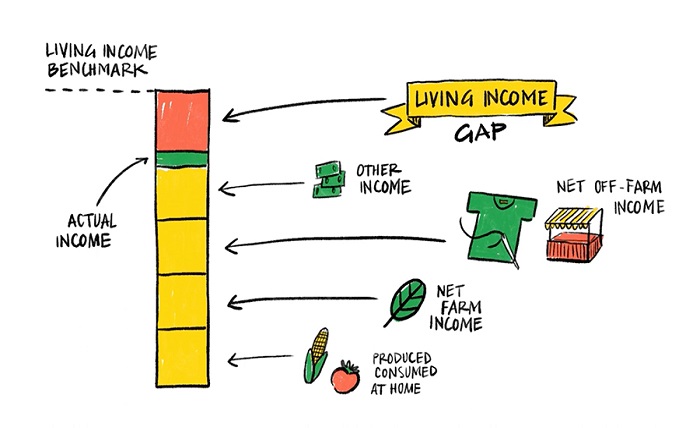

When a household knows it will receive subsidized grain each month, food expense becomes stable. The family can shift cash toward school fees or farm inputs. The support does not increase income, but it reduces pressure.

Predictable supply works like a fixed salary. It sets a baseline. Once the baseline exists, decisions become clearer. Savings, even small ones, become possible.

Chance-based income does not offer that base. It depends on uncertain outcomes. Some people compare this uncertainty to watching a desi league match, where results can change quickly and momentum swings without warning. That volatility may be exciting in sport. It becomes stressful when applied to daily livelihood.

In rural households, stress carries cost. When income fluctuates, families delay payments. They borrow at higher interest. They cut nutrition or postpone health visits. Short-term risk spreads into long-term damage.

Guaranteed support reduces this chain reaction. It protects essentials first. Food security lowers anxiety. Lower anxiety improves decision quality.

Planning power is not dramatic. It does not create headlines. But it builds resilience quietly.

Volatility And Its Hidden Costs

Volatile income affects more than cash. It affects behavior.

When earnings rise and fall sharply, households adjust quickly. They increase spending during good periods. They cut sharply during weak ones. This pattern creates instability.

Short-term gains often mask long-term risk. A sudden windfall feels strong. It may encourage larger purchases or informal lending. If the next month brings low income, the household struggles to balance.

Uncertain earnings also increase borrowing. When cash runs short, families rely on informal credit. Interest rates in such systems can be high. Debt grows faster than income.

Volatility changes food consumption patterns. In good months, meals improve. In bad months, portions shrink. This cycle affects health, especially for children.

Stress rises under unpredictable income. Stress reduces focus. It narrows thinking to immediate survival. Long-term planning fades.

These hidden costs accumulate. They do not appear in one dramatic event. They build slowly, through small compromises repeated over time.

Stable support systems reduce these compromises. They act as shock absorbers. Even if total income remains modest, predictability lowers risk.

Risk Management At The Household Level

Every household manages risk, whether formally or not.

Some risks come from weather. Others come from crop prices or health events. Income uncertainty adds another layer. When that layer grows, vulnerability increases.

Guaranteed support acts as a built-in hedge. It covers essential needs first. Food subsidy, for example, ensures that a bad income month does not become a hunger month. This protection stabilizes the base of the household budget.

With essentials secured, families can take measured risks. A farmer may invest in better seeds. A parent may support higher education. These choices depend on a stable floor.

Chance-based income reverses the sequence. The household first faces uncertainty. Then it tries to secure essentials. When income fails, risk multiplies.

Risk management improves when outcomes become predictable. Even partial predictability helps. Knowing that grain or subsidy will arrive reduces the need for emergency borrowing.

At the household level, stability is not about avoiding ambition. It is about sequencing it correctly. Secure basics first. Expand after.

Structured support systems enable this order. They do not eliminate risk. They contain it.

Long-Term Stability Builds Real Mobility

Mobility requires time. Time requires stability.

When a household meets basic needs without fear each month, it can think beyond the next week. Children attend school regularly. Health visits happen on schedule. Savings, even modest ones, begin to accumulate.

Guaranteed support creates this runway. It does not create wealth overnight. It prevents sudden collapse. That prevention matters more than short spikes in income.

Chance-based income rarely supports long-term plans. Large but uncertain gains cannot anchor steady investment. Families hesitate to commit to multi-year expenses when earnings swing.

Real mobility depends on consistency. Education requires years. Skill development requires patience. Asset building requires disciplined savings. These processes thrive under predictable conditions.

Stable support also strengthens community. When many households experience fewer shocks, local markets function better. Credit dependence drops. Informal stress declines.

This comparison is not about ambition versus caution. It is about foundation versus fluctuation.

Guaranteed support secures the floor. Once the floor holds, growth can rise. Without that floor, each step carries greater risk.

In rural households, resilience begins with predictability. Stability does not remove hardship. It makes hardship manageable.